Investing in Real Estate to Survive a Bear Market

Date: Oct 08, 2018 10:08 AM

Investing in Real Estate to Survive a Bear Market

With the S&P 500 near all-time highs, and the stock market experiencing the longest bull market in history, many investors are anxious. As a result, some of them are looking at residential real estate investments to protect themselves from a potential upcoming bear market.

High-quality bonds have historically provided a natural hedge for a market sell-off (Barclays Aggregate Bond Index has produced positive returns in each of the S&P 500's six negative calendar years since 1980). The bond index was up 5.2% in 2008 when the S&P 500 sold off 37% as a result of the housing/credit crisis. With interest rates on the rise and inflation creeping into the economy, many investors are wondering if allocating more capital to residential real estate is the best way to survive a potential bear market.

Real Estate in Bear Markets

Comparing residential real estate performance with the stock market in different historical periods provides some clues about whether or not real estate will help protect investments during the next bear market. During the eight bear markets since 1960, the Case-Schiller Home Price Index only had negative returns during one bear market period: the 2007-2009 housing/credit crisis. It’s interesting to note that home prices even went up during periods of high inflation, like the 1980-1982 bear market and 1973-1974 bear market, when the consumer price index (CPI) went up 14% and 20%, respectively.

Stock Market Versus Real Estate Returns

Over long periods of time, home prices have tended to follow a relatively predictable return pattern, increasing about 1% more per year than the CPI. The Case-Schiller index has returned 4.1% annually since 1980, compared to 3.1% for the CPI. While the stock market has done much better, returning 8.7% per year since 1980, its performance has varied dramatically. The annual return for the S&P 500 was 4.4%, 1.7%, 12.5%, 15.1%, and -2.5% in the 1970s, 1980s, 1990s and 2000s, versus an annual home price growth of 8.7%, 5.9%, 2.7%, and 3.9% in those same years. Home price growth has had a significantly lower standard deviation of returns. For example, the standard deviation of the Case-Schiller index is less than 20% of the standard deviation of the S&P 500. (For related reading, see: Understanding the Case-Schiller Index.)

S&P 500 and Case-Schiller: An Imperfect Comparison

While the data shows us real estate still performs well in bear markets and experiences less volatility in its returns, drawing conclusions from the S&P 500 and the Case-Schiller Home Index presents some issues. The housing return data doesn’t include rent on a home, so comparing the total returns between the S&P 500 and Case-Schiller is imperfect.

Real estate’s low volatility may be overstated due to the higher transacation costs and the period of time it takes to convert a property into cash. Since buying and selling real estate costs so much in terms of time and transaction costs, real estate investors don’t trade as often as stock investors do, and they are less likely to engage in irrational and impulsive buy-and-sell decisions.

Stock investors have the ability to sell their securities with the click of a button, and at a low cost. This ease of selling means stock investors can quickly fall victim to emotional investing. They are more likely to buy at market tops as a result of greed, and sell at market bottoms because of fear. This emotion-driven market timing causes investors to dramatically underperform the indexes, as evidenced in the 2017 Dalbar study which concluded that equity investors underperform stock indexes by 2.9% annually over a 20-year period. If investors were able to buy and sell individual real estate properties on a public exchange without high transaction costs, there would likely be much higher volatility in returns. (For related reading, see: Financial Markets: When Fear and Greed Take Over.)

Price Anchoring to Avoid a Loss

The return data for the Case-Schiller Home Index over short periods of time is also questionable. For example, there’s a tendency for investors who want to sell in a down market to “anchor” the price they want to sell at to a level that is above their original purchase price. They may also try to avoid taking a loss by delaying selling until the recessionary period is over, and they’re more likely to sell the property for more than they paid initially. This can create an artificial floor in real estate prices and skew the return data. Since the Schiller-Case data is based on actual sales, a real estate downturn and lower housing demand won’t show up in the data unless a sale is actually made.

Scenarios When Real Estate and Bear Markets Work

Real estate most likely will not sidestep an entire bear market, but it can definitely benefit investors during a downturn in certain scenarios. If a bear market coincides with a period of a high inflation like it did in the 1970s, real estate is probably a good bet. Bonds, which most people use as a hedge against a bear market, performed very poorly during the 1970s.

If you know you're the type of investor who reacts emotionally during a market downturn, and as a result experience poor market timing and underperformance, real estate may make sense for you. The high transaction costs and barriers to selling will help you stay invested and earn better returns in the long run.

Maximizing Your Returns

When it comes to real estate investing, it’s important to clearly articulate your investment plan and understand the competitive advantage you have to execute that plan. There are a lot of ways to make money in real estate, and the most successful investors know what their edge is and how to maximize it. For some investors, their edge could be a lower cost of financing, while for others it could be be identifying areas with surging demographic trends before other investors drive up prices. (For related reading, see: Making Money in Residential Real Estate.)

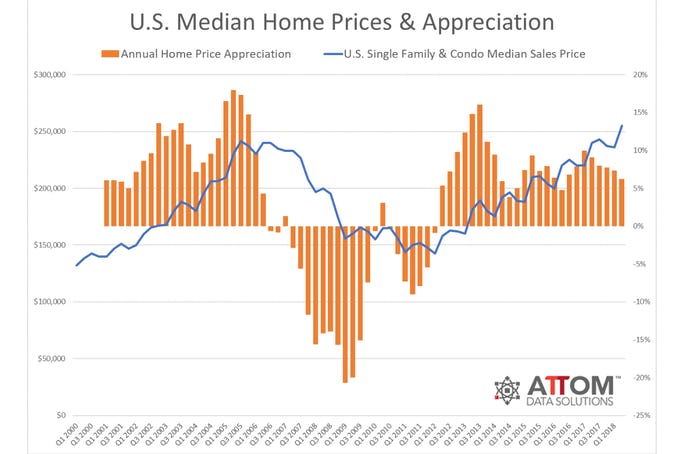

For example, your real estate investment plan may include taking advantage of positive demographic trends: an area with a lot of new businesses and job creation can help the real estate market in the short and long term. (For example, markets like Denver, Nashville and Austin). While real estate has performed well during recessions in the past, prices and valuation matter. In 2018, the Case-Schiller Home Index is 10% higher than it’s pre-housing crisis peak in July 2006. Finding a property that has good growth potential and a high level of income relative to price is increasingly important whenever there are market peaks.

Trend Forecasting Is Challenging in Real Estate

Real estate performance is local, so it can be difficult to forecast overall trends and returns for real estate. There’s wide dispersion for real estate returns depending on the area, property type, neighborhood, etc. For example, the Washington, DC residential real estate market continued to expand in the years after the 2008 financial crisis due to massive government spending and strong job growth in the government sector. On the other hand, the Miami condo market contracted sharply during this time. Property types react very differently to a bear market.

Vacation homes and the ultra-luxurious sectors are likely to contract greater than the typical residential property. A shrewd real estate investor can increase his or her chances of side-stepping a bear market by picking the right properties.

Don't Drastically Change Your Portfolio in Preparation for a Correction

Before doing something drastic, like trying to time a bear market by re-allocating the bulk of your investment portfolio into real estate, it’s important to recognize that market corrections and bear markets are normal. There have been 29 market corrections (declines of 10%) and bear markets (declines of 20%) since 1960. Drawing on historical data, investors can expect a 10% selloff every 2.8 years and a 20% selloff every 7.3 years. And while there have been five market corrections since the last bear market (2007-2009), bear markets should not be feared.

The patient investor will continue to make money in the market over long periods of time. Patience is a better indicator for investing success than market timing.

(For related reading, see: Reasons to Invest in Real Estate Versus Stocks.)

Source: https://www.investopedia.com/advisor-network/articles/investing-real-estate-survive-bear-market/